Introduction

Your credit score is the most important thing you will have with you for the rest of your life. It affects almost every large purchase you make, but it can also affect almost every small purchase you make. So, what exactly is a credit score, what does it affect, what is the average credit score in America, and what are the basic statistics and facts about a credit score?

In this article, we’ve gathered all the information you need on credit scores in the United States.

9 Brisk Credit Score Facts and Statistics

- In the United States, the average credit score is 716.

- The average credit score for people aged 23 to 29 in the United States is 660.

- The average credit score for those aged 80 to 89 is 757.

- The median credit score for low-income families is 658.

- Asian Americans have the greatest credit score of any race, with a score of 745.

- At 677, black Americans have the poorest credit score of any race.

- Men have marginally higher credit scores than women.

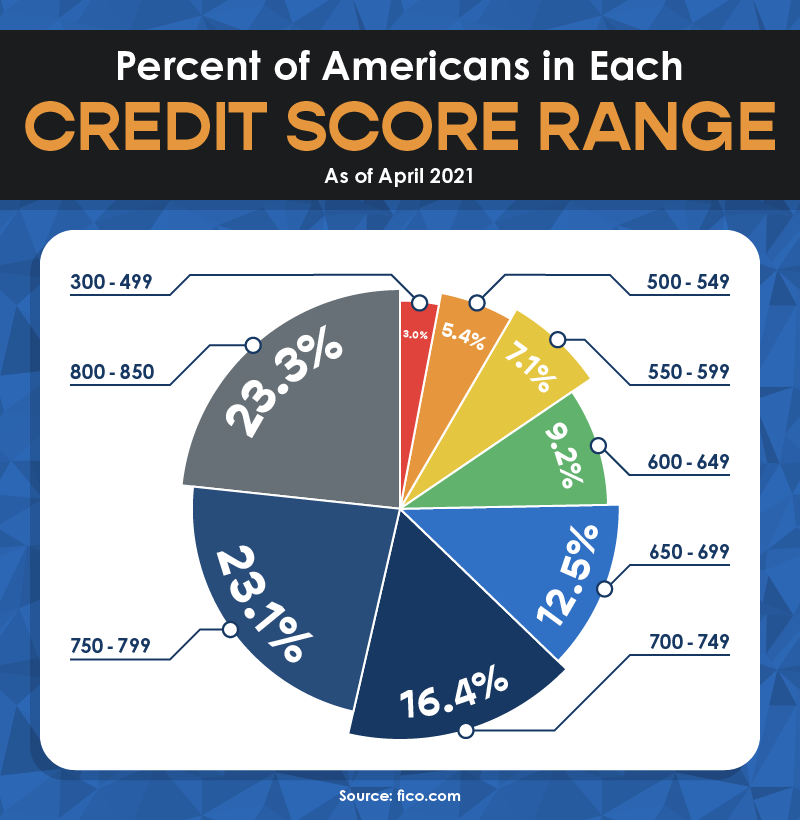

- 23.3% of the US population have credit scores ranging from 800 to 850.

- 35% of your credit score is determined by your record of payments.

Average Credit Score in the U.S. – What Is it?

- Overall Score – FICO reports that the average credit score in America sits at 716, 8 points higher than in October 2020, indicating a strong credit standing. This information helps understand where your credit stands in the country.

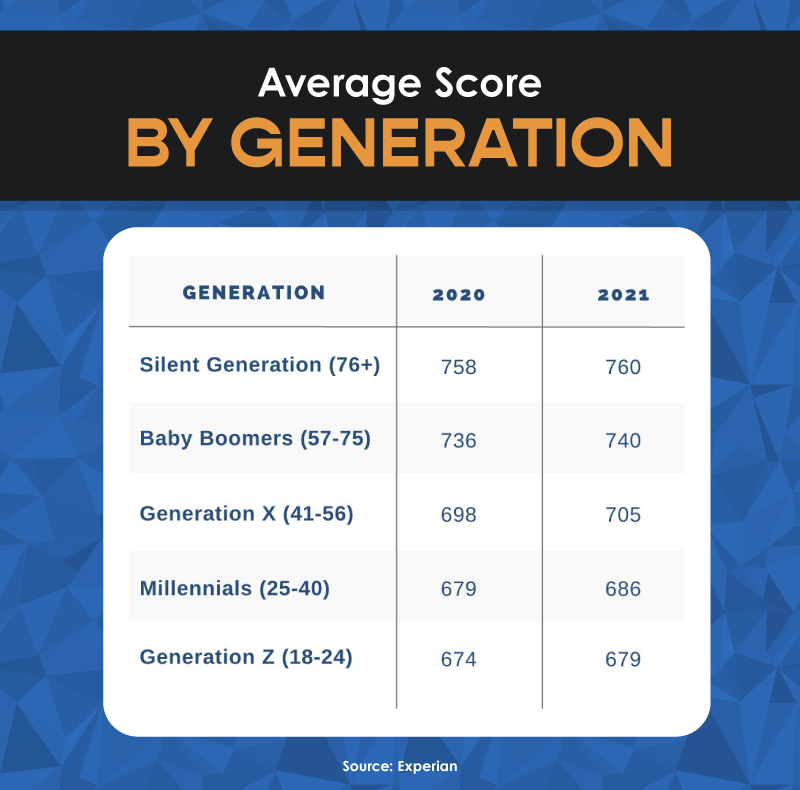

- Average Score by Age – Due to the build-up of credit over the years, youngsters have lower credit scores. According to Experian, average credit ratings rise with age, with younger generations having higher scores on aggregate.

- Average Score by Income – The median credit score for low-income families is 658, the median credit score for moderate-income families is 692, the median credit score for middle-income families is 735, and the median credit score for families with substantial incomes is 774. Loan ratings, which are essential for obtaining loans and basic necessities, have a strong correlation with income. Households with lower incomes and median credit scores of 658 would have less affordable access to credit than households with scores of 720 or higher.

- Average Score by Gender & Race – Men’s average credit scores are slightly higher than women’s. Males’ average credit score ranges from 781 to 774, while females’ average credit scores range from 745 to 774, with Asians having the highest average score (745) and blacks having the lowest average score (677). Non-Hispanic whites score 734, while Hispanic whites score 701 and all others score 732.

Average U.S. Credit Score Ranges

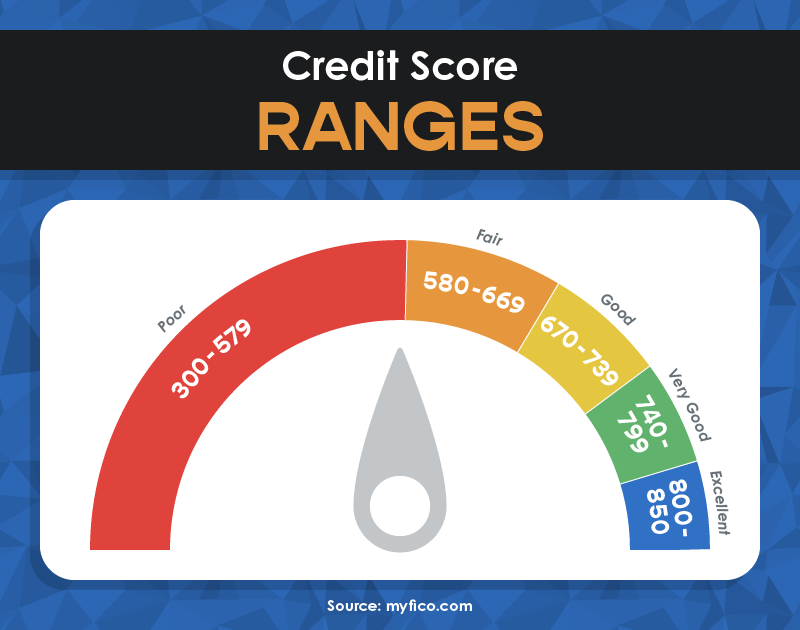

A credit score is a numerical indicator of an individual’s ability to repay loans on time. It is calculated using information from the individual’s credit report and is typically between 300 and 850 points. The higher the score, the greater the assurance lenders have that the individual is responsible and more likely to be approved for a loan.

Score ranges and their meaning: American customers’ credit scores vary significantly, with poor scores being hazardous, fair scores being acceptable, decent scores being close to or slightly above the national average, and very good scores being rare. The national average for American customers is 740 to 799, while the average for American consumers is 800 to 850. Despite these differences, lenders generally approve loan applications for American customers.

The calculation of a credit score is based on data from an individual’s credit report, such as payment history, outstanding debt, and the duration of their credit history. However, there are various scoring models that take into account a variety of factors. As of April 2021 data, the majority of US citizens fall into one of the following credit score ranges –

Who Will Check Your Credit and Why?

A good credit score is crucial for lenders to assess a borrower’s ability to repay loans. Creditors use hard credit checks, also known as hard inquiries, to determine loan approval. Soft inquiries, also known as background checks, are used by businesses for situations like credit card offers or housing applications. These inquiries are unaffected by your credit score, but it is essential to examine your own credit before submitting personal details for a soft credit check. It is also crucial to verify the integrity of a website before submitting personal details for a soft credit check.

Different Credit Scoring Models

- FICO – 90% of leading lenders use FICO scores, which were developed by Fair Isaac Corporation, to determine creditworthiness. The data in a consumer’s credit report, which is kept up to date by the three major credit agencies Equifax, Experian, and TransUnion, is used to determine these scores. By comparing this data to trends in hundreds of thousands of previous credit reports, FICO scores forecast future credit risk. Five types of data from credit reports are used to create FICO scores: payment history (35%), credit utilisation (30%), duration of credit history (15%), credit account mix (10%), and new accounts (10%).

- VantageScore – It is a well-known consumer credit scoring methodology that was created by Equifax, Experian, and TransUnion in 2006. It rates six categories of data from credit reports and describes the strength of each category’s influence. Payment history, credit utilisation, history duration, amounts owed, recent credit behaviour, and credit availability are all significant factors. The FICO score methodology has less impact.

How To Improve Your Credit Score?

Prioritise on-time payments, reduce balances on revolving credit cards, take care of past-due accounts, and restrict credit applications to raise your credit score. The quantity, kind, and existing score of your negative marks will determine how long it will take to raise it. As you begin to pay off debts, be patient and make tiny instalments because missed payments have a lower impact.